News

21 January 2026

Time to review 2020 and prognosticate on 2021. Around this time last year we wrote a piece titled “2019 A Surprisingly Good Year for Risk Assets: 2020 Outlook,” time to do it all again. The cautious stance looked ok, even before Covid-19 kicked in and reduced the global economy to an effective standstill. Our stance on Japan was positive and we continued to bemoan the lack of incentives on the fiscal side and we wanted the cessation of the ‘monetary policy for rich people’ aka Zero Interest Rate Policy.

This article was originally published on TAMIM. Reach Markets has permission from the author to publish it. The views and opinions expressed in this article are those of the author and do not necessarily reflect the views and opinions of Reach Markets.

Time to review 2020 and prognosticate on 2021. Around this time last year we wrote a piece titled “2019 A Surprisingly Good Year for Risk Assets: 2020 Outlook,” time to do it all again.

The cautious stance looked ok, even before Covid-19 kicked in and reduced the global economy to an effective standstill. Our stance on Japan was positive and we continued to bemoan the lack of incentives on the fiscal side and we wanted the cessation of the ‘monetary policy for rich people’ aka Zero Interest Rate Policy. Someone might be listening because we now have a plethora of fiscal incentives being discussed, which should (finally) help to improve productivity and growth potential on a sustainable basis. Check out the (lack of) GDP per capita growth in most Western style economies if you believe ZIRP has produced anything other than a reflated asset souffle; and MUCH more debt risk.

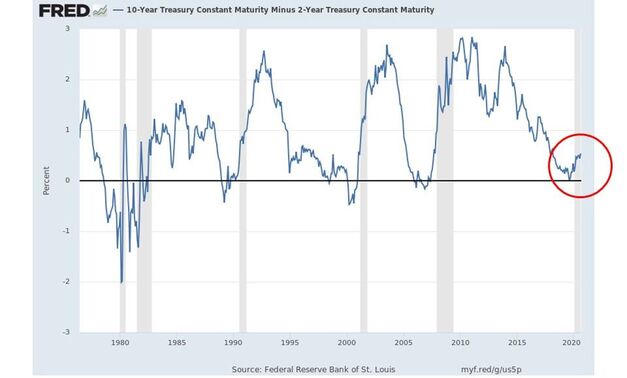

Speaking of debts. The COVID-19 response has shovelled more debt onto future generations. This can’t be paid back, shouldn’t be paid back, and so won’t be paid back. Currently inflation is everyone’s good idea (not ours) of the way to deal with this overhang. Let’s just say that:- it’s risible that policy makers believe that exactly the right amount of inflation can be created; that it will inflate away the value of debts to the benefit of only the most deserving indebted; and that it can immediately be bottled up when the correct amount of debt destruction has been reached.

If there is too much debt (and there is) and you think that some segments of society deserve a reprieve then a MUCH BETTER WAY is to have focused debt forgiveness and write it off. The incoming (?) Biden administration is examining writing off significant amounts of student debt. We would also politely suggest that the Virtue Signaling ‘Tech Luvvies’ might also think about having their companies pay some tax? We see that Mr Musk has moved to Texas because of the apparent “lack of support for tech industries now in California”.

Hah- Oh yeah? Nothing to do with significant differences in state tax and their likely trajectories then? A dirty little secret of the Trump administration is that he RAISED taxes significantly through reductions in offset allowances between state and federal filings. This hit the Democrat states hardest and the population shift South and East in the USA is quite remarkable.

2020 was ok and the best thing we did was to not panic in April and remain invested. It’s our investment philosophy that timing markets, risk factors and style shifts is difficult and dangerous.

So, what do we make of 2021? Here’s some thoughts and they are brief because we know everyone has a crystal ball out at the moment. However, ours ARE definitely 100% correct.*

Click here to join our next ‘The Insider: Meet the Fund Manager’ session, a FREE webcast series gives you direct access to prominent fund managers who share their “Insider” views on their top stock picks that they think have the greatest upside.

Past performance is not a reliable indicator of future performance.