Analyst Research

14 August 2019

AZJ reported FY18 results as expected. Key highlights include EBIT up 6% to $940.6m driven by: (1) Coal up $8.6m (2%) on +7% higher volumes but partly offset by higher costs due to price escalation and costs to add capacity to deliver further volumes;

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 14/08/18 | AZJ | A$4.48 | A$3.98 | NEUTRAL |

| Date of Report 14/08/18 | ASX AZJ |

| Price A$4.48 | Price Target A$3.98 |

| Analyst Recommendation NEUTRAL | |

| Sector : Transportation & Logistics | 52-Week Range: A$4.11 – 5.49 |

| Industry: Industrials | Market Cap: A$8,756.6m |

Source: Bloomberg

We rate AZJ as a Neutral for the following reasons:

We see the following key risks to our investment thesis:

Figure 1: AZJ EBIT by segment

Source: FY18 Company reports

Figure 2: AZJ Rail Haulage Operation

Source: Company

AZJ reported FY18 results as expected. Key highlights include EBIT up 6% to $940.6m driven by: 1. Coal up $8.6m (2%) on +7% higher volumes but partly offset by higher costs due to price escalation and costs to add capacity to deliver further volumes; 2. Bulk up $64.5m due to transformation benefits and lower depreciation from prior year impairments, partly offset by lower volumes; 3. Network was flat at $480.6m with operating cost savings offset by non-recurrence of UT4 true-ups in prior year.

AZJ also completed its $300m buy-back in 2H18. 4. Final dividend of 13.1cps is 60% franked (and equates to 100% payout of underlying NPAT from continuing operations), up +47% versus prior year; 5. AZJ achieved its three-year transformation target of $380m with $133.6m in benefits delivered, including importantly removed Intermodal’s FY17 losses (mainly related to Intermodal Interstate); 6. Australian Competition and Consumer Commission (ACCC) blocked the sale for the Queensland Intermodal business and Acacia Ridge Terminal and has commenced proceedings in the Federal Court.

The ACCC has also sought an injunction to prevent Aurizon from closing its Queensland Intermodal business while proceedings are on foot. The attractive yield of approximately 4.1% may keep some investors interested in the stock, however we see the stock in a trading range. Neutral.

ASK THE ANALYST

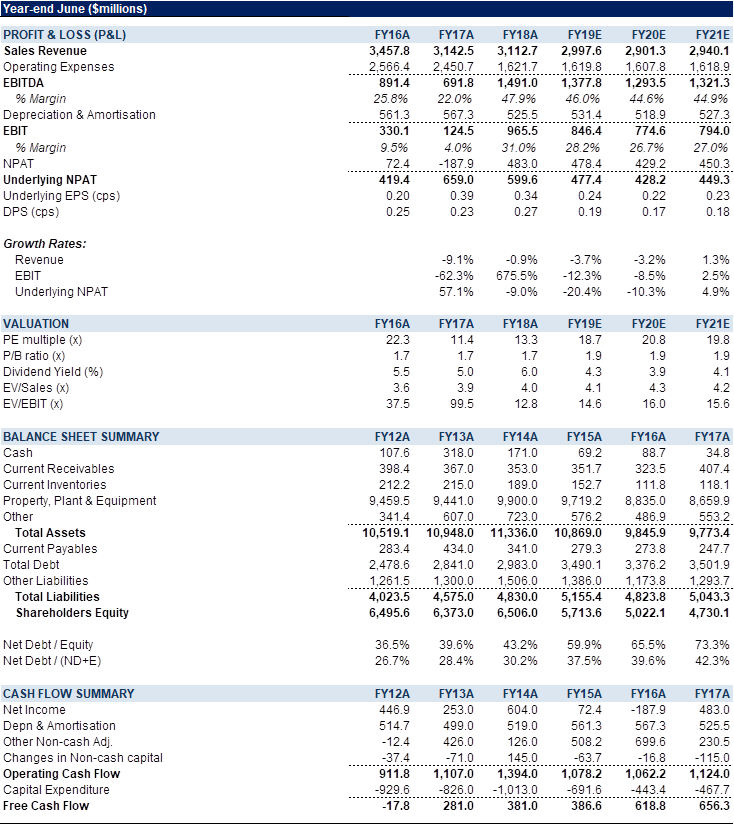

Figure 3: AZJ Financial Summary

Source: BTIG, Company, Bloomberg

Aurizon Holdings Ltd (AZJ) operates an integrated heavy haul freight railway in Australia. It transports various commodities, such as mining, agricultural, industrial and retail products; and retail goods and groceries across small and big towns and cities, as well as coal and iron ore. The Company also operates and manages the Central Queensland Coal Network that consists of approximately 2,670 kilometres of track network; and provides various specialist services in rail design, engineering, construction, management, and maintenance, as well as offers supply chain solutions. In addition, it transports bulk freight for customers in the resources, manufacturing, and primary industries sectors. The Company was formerly known as QR National Limited and changed its name to Aurizon Holdings Limited in December 2012. AZJ is headquartered in Brisbane, Australia.