Analyst Research

14 August 2019

ORG’s share price took a hit post FY18 results release, with management expecting FY19 Energy Markets EBITDA of $1.5bn – 1.6bn, indicating a 12-17% decline year-on-year and well below consensus estimates.

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 20/08/18 | ORG | A$8.89 | A$9.90 | BUY |

| Date of Report 20/08/18 | ASX ORG |

| Price A$8.89 | Price Target A$9.90 |

| Analyst Recommendation BUY | |

| Sector : Energy | 52-Week Range: A$6.96 – 10.27 |

| Industry: Oil, Gas & Consumable Fuels

| Market Cap: A$15,245.6m |

Source: Bloomberg

We rate ORG as a Buy for the following reasons:

We see the following key risks to our investment thesis:

ORG’s share price took a hit post FY18 results release, with management expecting FY19 Energy Markets EBITDA of $1.5bn – 1.6bn, indicating a 12-17% decline year-on-year and well below consensus estimates.

APLNG continues to perform in line with expectations and the long-term outlook for that business remains positive. Further, management noted that subject to market conditions, the Board will look to introduce dividends in FY19 (in line with our expectations).

We maintain our Buy recommendation given the improving debt position of the Company, improving cash flows (with APLNG providing significant delta) and reinstatement of dividends in FY19.

Whilst we concede Energy Markets business is facing challenges, we believe within the FY19 guidance, the Company has largely re-based earnings expectations. In due course, we believe investors will refocus on the significant cash flow opportunity from APLNG and returning dividends profile.

Figure 1: FY18 key headline numbers

Source: Company

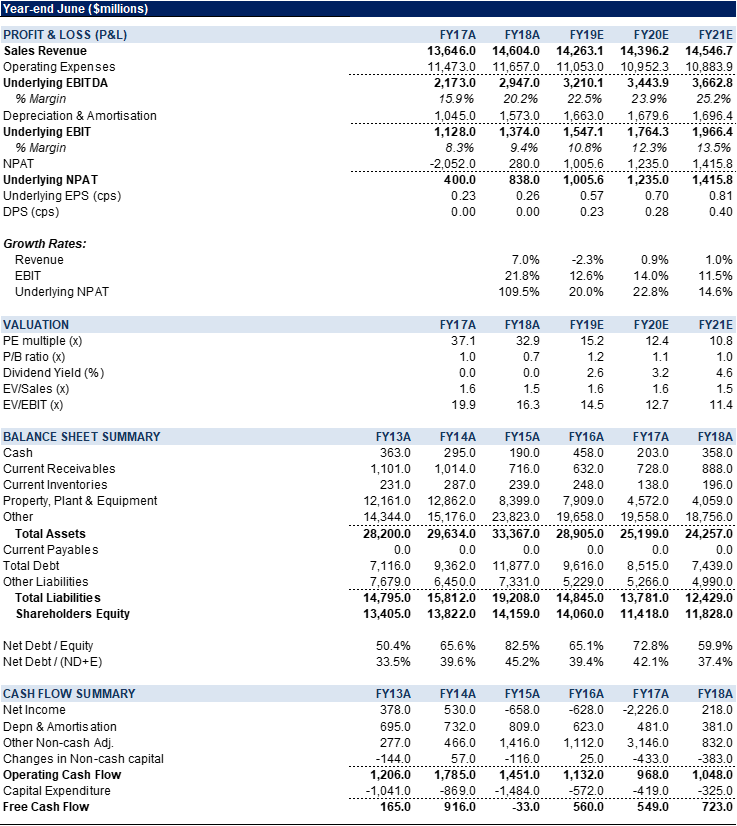

Figure 2: ORG Financial Summary

Source: BTIG, Company, Bloomberg

Origin Energy (ORG) is an integrated energy company with operations in exploration, production, generation and the sale of energy to millions of households and businesses across Australia. The Company has extensive operations across Australia and New Zealand, and pursuing opportunities in the fast-growing energy markets of Asia and South America. The Company has two main segments: 1. Energy Markets – retail sales of electricity, gas and other customer solutions; electricity generation; and wholesale trading of electricity and gas. 2. Integrated Gas – consists of upstream exploration, development and production; the segment also holds the 37.5% ownership in Asia Pacific LNG project.