Analyst Research

14 August 2019

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 09/08/18 | LEP | A$5.50 | A$5.20 | NEUTRAL |

| Date of Report 09/08/18 | ASX LEP |

| Price A$5.50 | Price Target A$5.20 |

| Analyst Recommendation NEUTRAL | |

| Sector : Financials | 52-Week Range: A$4.52 – 5.83 |

| Industry: REIT | Market Cap: A$1076.7m |

Source: Bloomberg

We rate LEP as a NEUTRAL for the following reasons:

We see the following key risks to our investment thesis:

Figure 1: : Properties by State

Source: BTIG, Company

Figure 2: : Property value by state

Source: BTIG, Company

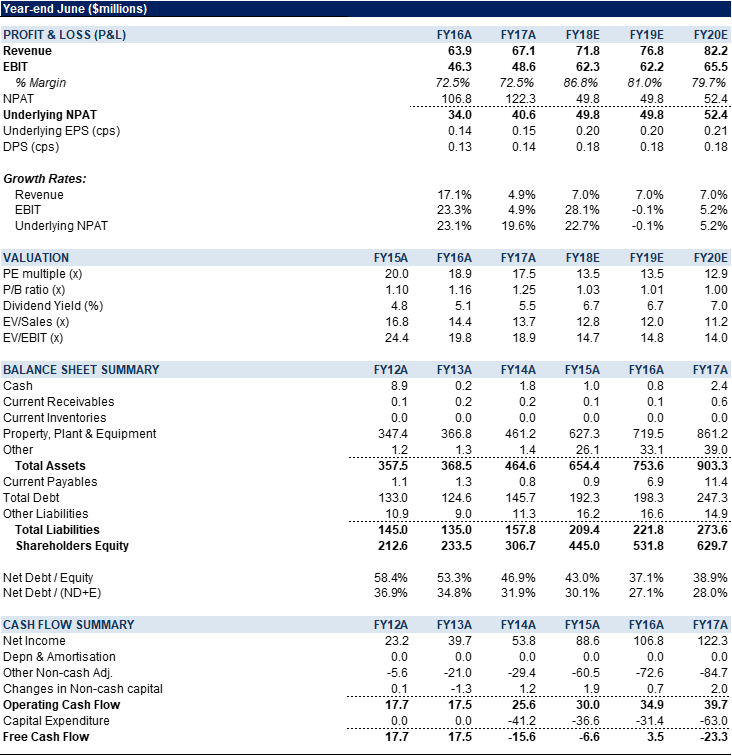

ALE Property Group (LEP) reported solid but as expected FY18 results.

Key highlights to FY18 results included:

1. increased distributions by ~2.0% to $29.0m (or 20.8cps) – in line with manager expectations;

2. Weighted average adopted cap rate reduced from 5.14% to 4.98%;

3. Directors’ valuation of 86 properties increased by 5.0% to $1,136.3m;

4. Market rent review of 80 properties has commenced for FY19 and is expected to deliver a positive result;

5. Balance sheet remains solid with gearing at historic low of 41.6%, debt maturities diversified over the next 5.4 years and net debt 100% hedged for next 7.4 years with current all up cash interest rate of 4.26%;

6. FY18 property revenue of A$58.1m over the previous year, up +1.9% (driven by annual CPI based rent increases).

7. Weighted Average lease expiry was 10.3 years with the portfolio at 100% occupancy.

LEP is no doubt a quality business, with strong management team, strong property portfolio and solid balance sheet – We retain our Neutral recommendation on valuation grounds.

ASK THE ANALYST

Figure 3: LEP Financial Summary

Source: Company

Figure 4: LEP Financial Summary

Source: Company,BTIG, Bloomberg

ALE Property Group (LEP) is the owner of Australia’s largest portfolio of freehold pub properties. Established in November 2003, ALE owns a portfolio of 86 pub properties across Australia, with a value of ~$1,080m (average value of $12.6m on weighted average cap rate of 5.14%). All the properties are leased to Australian Leisure and Hospitality Group Limited (ALH).