Analyst Research

14 August 2019

Bapcor Ltd (BAP) FY18 results were largely in-line with consensus estimates, with proforma NPAT of $86.5m coming in consensus range of $85.2m-90.3m which saw the stock price increase marginally.

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 24/08/18 | BAP | A$6.95 | A$6.74 | NEUTRAL |

| Date of Report 24/08/18 | ASX BAP |

| Price A$6.95 | Price Target A$6.74 |

| Analyst Recommendation NEUTRAL | |

| Sector : Consumer Discretionary | 52-Week Range: A$5.19 – 7.24 |

| Industry: Distributors | Market Cap: A$1,939.3m |

Source: Bloomberg

We rate BAP as a Neutral for the following reasons:

We see the following key risks to our investment thesis:

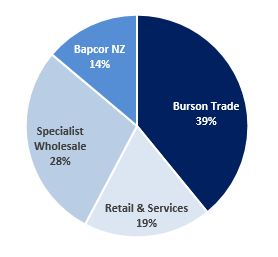

Figure 1: Revenue by segment

Source: Company

Source: Company

Bapcor Ltd (BAP) FY18 results were largely in-line with consensus estimates, with proforma NPAT of $86.5m coming in consensus range of $85.2m-90.3m which saw the stock price increase marginally.

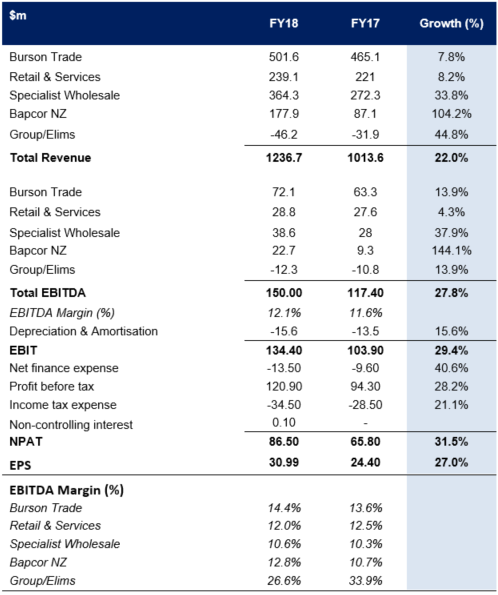

Key financial highlights (including the Hellaby business) versus the previous corresponding period (pcp): 1. revenue up +22% to $1.23bn; 2. Underlying EBITDA growth of +28% to $150m; 3. Proforma NPAT up +31.6% to $86.5m; and 4. EPS at 30.99cps (a +27% increase), indicating healthy organic growth in the underlying business.

Management declared a final fully franked dividend of 8.5 cents per share (up 13.3% compared to the pcp), bringing the total dividends for FY18 to 15.5 cps (up 19.2%). Further, management noted that consensus estimate of FY19 EBITDA of $170m was reasonable and they expect an increase in NPAT of 9%-14% above FY18 proforma NPAT.

We maintain our Neutral recommendation only on valuation grounds only but note management guidance of a strong year ahead (our numbers are on the lower end of guidance or on the conservative side).

Figure 3: Segment results

Source: Company

Figure 4: BAP Comparables

Source: Company

Figure 5: BAP Financial Summary

Source: Company

Bapcor Ltd (BAP) is Australasia’s leading provider of aftermarket parts, accessories and services. The core businesses of BAP are: 1. Trade – Burson Auto Parts is a trade focused parts professional supplying workshops with all their parts and accessories. 2. Retail – Autobarn is the premium retailer of auto accessories and Opposite Lock specialises in 4WD accessory specialists. 3. Independents – supporting the independent parts stores via the group’s extensive supply chain capabilities and through brand support. 4. Specialist Wholesaler – the number 1 or 2 industry category specialists in parts supply programs. 5. Services – experts at car servicing through Midas and ABS.