Analyst Research

14 August 2019

CSL continues to deliver pleasing results, coming in slightly ahead of guidance posted in May, with FY18 earnings (NPAT) up +29% on the previous corresponding period (pcp) (or up +28% on a constant currency, CC basis).

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 16/08/18 | CSL | A$214.17 | $222.50 | BUY |

| Date of Report 16/08/18 | ASX CSL |

| Price A$214.17 | Price Target $222.50 |

| Analyst Recommendation BUY | |

| Sector : Healthcare | 52-Week Range: A$119.01 – 205.03 |

| Industry: Biotechnology | Market Cap: A$91,244.7m |

Source: Bloomberg

We rate CSL as a Buy for the following reasons:

We see the following key risks to our investment thesis:

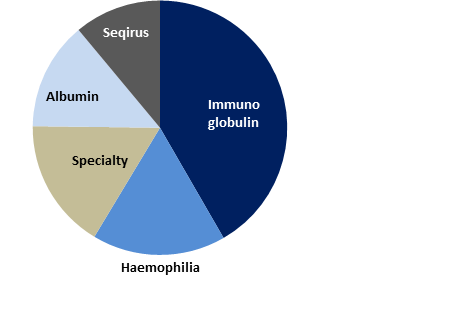

Figure 1: CSL Revenue by Product

Source: Company

Source: Company

CSL continues to deliver pleasing results, coming in slightly ahead of guidance posted in May, with FY18 earnings (NPAT) up +29% on the previous corresponding period (pcp) (or up +28% on a constant currency, CC basis).

The key highlight was CSL’s flu business (Seqirus) posting its first year of EBIT contribution, however, overall, all primary therapies across both segments posted sales growth.

Given the strong operating performance and management FY19 guidance, we have upgraded our estimates. We maintain our Buy recommendation and see further upside to current share price.

ASK THE ANALYST

Figure 3: P&L summary

Source: BTIG, Company

Figure 4: CSL comps table – consensus estimates

Source: BTIG, Bloomberg

Figure 5: CSL Financial Summary

Source: BTIG, Company, Bloomberg

CSL Limited (CSL) develops, manufactures and markets human pharmaceutical and diagnostic products from human plasma. The company’s products include paediatric and adult vaccines, infection, pain medicine, skin disorder remedies, anti-venoms, anticoagulants and immunoglobulins. These products are non-discretionary life-saving products.