Analyst Research

14 August 2019

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 21/08/18 | NHF | A$6.44 | $6.32 | NEUTRAL |

| Date of Report 21/08/18 | ASX NHF |

| Price A$6.44 | Price Target $6.32 |

| Analyst Recommendation NEUTRAL | |

| Sector : Financials | 52-Week Range: A5.13 – 7.2 |

| Industry: Life and Health Insurance | Market Cap: A$2,997.5m |

Source: Bloomberg

We rate NHF as a Neutral for the following reasons:

We see the following key risks to our investment thesis:

Figure 1: Revenue by segment

Source: Company

Source: Company

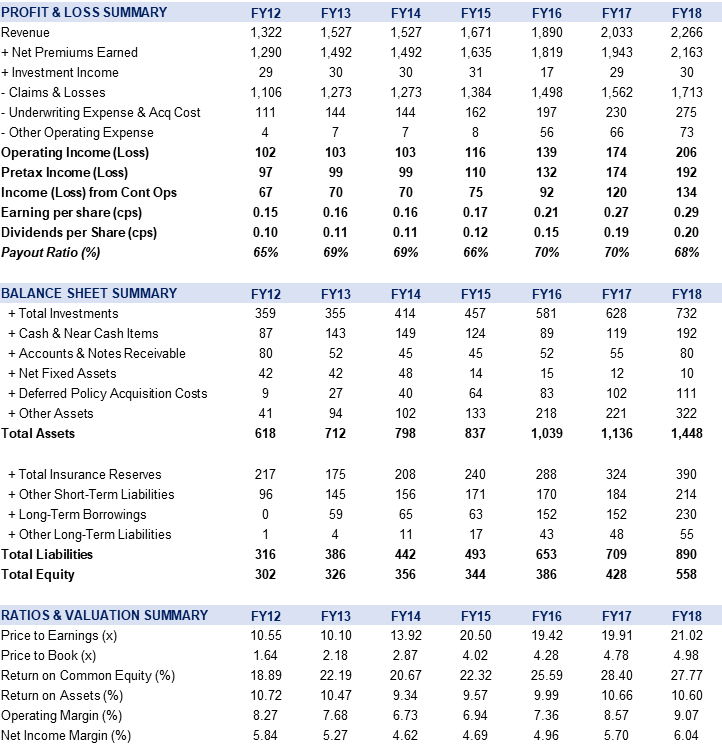

nib Holdings Limited (NHF) announced FY18 results delivering underlying operating profit (UOP) of $184.8m, an increase of +20.2% on the pcp. Net profit after tax (NPAT) grew +11.1% to $133.5m but missed analyst estimate of $135m which saw NHF’s share price slide by -1.8%.

Statutory earnings per share were up by +8.0% to 29.4cps. Management declared a final dividend of 11cps, increasing the full year dividend for FY18 to 20cps (fully franked), representing a gain of +5.3% on payout ratio of 68.5%.

We see nib as having attractive growth avenues through their current JV with Tasly, which would provide an opportunity to sell health insurance in China, however increasing regulatory scrutiny and difficult market conditions in Australia and NZ are likely to have a negative impact on margins and profits in the short term (whilst the long-term investment thesis remains intact). Trading on PE-multiple of 19.7x and yield of 3.2% – maintain Neutral.

Figure 3: NHF Financial Summary – by segments

Source: Company, BTIG, Bloomberg

Figure 4: FY19 Guidance Breakdown

Source: Company, BTIG, Bloomberg

Figure 5: Australian Insurance Comparable

Source: Company, BTIG, Bloomberg

Figure 6: NHF Financial Summary

Source: Company, BTIG, Bloomberg

nib Holdings Limited (NHF) is the Australian private health insurer. NHF operates in four divisions which are private health insurance, life insurance, travel insurance and related health care activities.