Analyst Research

14 August 2019

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 10/08/18 | ORA | A$3.46 | A$3.55 | NEUTRAL |

| Date of Report 09/08/18 | ASX ORA |

| Price A$3.46 | Price Target A$3.55 |

| Analyst Recommendation NEUTRAL | |

| Sector: Materials | 52-Week Range: A$2.87 – 3.73 |

| Industry: Containers & Packaging | Market Cap: A$4,211.3 |

Source: Bloomberg

We rate ORA as a Neutral for the following reasons:

We see the following key risks to our investment thesis:

ORA’s FY18 underlying NPAT of A$208.6m was up +12% on previous corresponding period (pcp), slightly ahead of consensus estimates of A$206.6m. However, at the operating earnings line (EBITDA) the company missed consensus estimates by approximately 2%, driven by weakness in the North American business.

North American segment saw EBIT margin decline by ~20bps to 5.6% reflecting the impact of doubtful debt provision in Orora Visual and transitional costs associated with the ERP system in OPS. The Australasia business was a standout (EBIT up +8.7% on pcp & margins up +30bps), delivering strong earnings growth despite higher energy costs.

On a positive note, ORA signed two separate power purchase agreements (PPA) with renewable energy providers to supply wind-generated electricity to ORA’s operations in South Australia, Victoria and New South Wales, securing competitive long-term supply of renewable energy for volumes equivalent to 80% of ORA’s total electricity requirements in Australia. Whilst absent in recent periods, management noted that bolt-on M&A was back in focus as a source of growth driver, with a healthy pipeline of targets built up over the past 5-6 months.

With a solid balance sheet (net debt/EBITDA at 1.5x), management has A$354m in undrawn bank debt capacity to fund acquisitions in their A$75-125m preferred range. Further we highlight ORA’s leverage to a falling Australian dollar, with +/-1 cent movement in AUD/USD equating approx. -/+$1.6m impact on EBIT and -/+$1.0m on NPAT.

1. disappointing earnings outcome in the North American business, with EBIT margins declining 20bps on pcp. As a consequence, the Company missed consensus estimates by ~2% for FY18 at the operating earnings line (EBITDA).

2. A key component of ORA’s growth strategy is bolt-on acquisitions and the absence of any M&A announcement may have disappointed the market. Management noted the ERP rollout and the integration of OV had occupied their focus. However, in our view, the positive was that ORA delivered solid organic growth in FY18, driven by internal investments.

3. Cash conversion was lower on pcp and likely to be lower again in FY19.

ASK THE ANALYST

Figure 1: : ORA Revenue by Segment

Source: BTIG, Company

Figure 2: : ORA EBIT by Segment

Source: Company; North America in AUD currency

Figure 3: Group FY18 key trading metrics

Source: BTIG, Company, Bloomberg

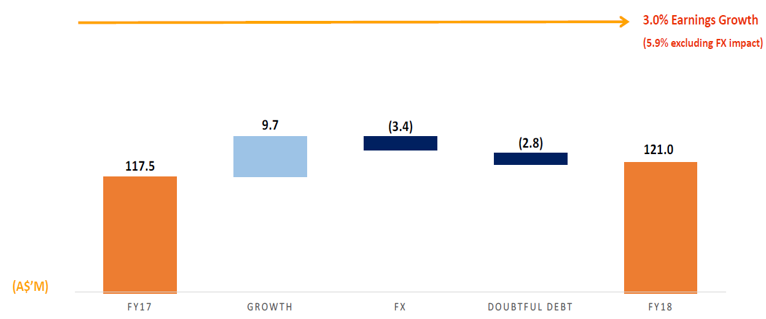

Figure 4: FY18 Australasia earnings (EBIT) drivers

Source: BTIG, Company, Bloomberg

Figure 5: FY18 North America earnings (EBIT) drivers

Source:Company

We value ORA using three methods: DCF (A$3.81), EV/EBITDA (A$3.70) and PE-relative (A$3.26). Our 5-year forecasts assume on a CAGR basis: revenue growth of +4.4% p.a., operating earnings growth of +6.0%; and EPS growth of +7.8% p.a. For our relative valuations, we use peer group consensus estimates for ORA, Amcor (AMC) and Pact Group (PGH). We arrive at a price target of A$3.55, which is the average of our three valuations (rounded to the nearest five cents). On our estimates for FY19, ORA is trading on a PE-multiple of 18.9x and yield of approximately 3.7%.

Figure 6: ORA Financial Summary

Source: BTIG, Company, Bloomberg

Orora Limited (ORA) provides packaging products and services. The Company offers fiber, glass and beverage can packaging materials in Australia and Asia and packaging distribution services in North America and Australia.