Analyst Research

14 August 2019

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 22/08/18 | PRY | A$2.75 | A$2.43 | SELL |

| Date of Report 22/08/18 | ASX PRY |

| Price A$2.75 | Price Target A$2.43 |

| Analyst Recommendation SELL | |

| Sector: Healthcare | 52-Week Range: A$2.90 – 3.97 |

| Industry: Healthcare Services | Market Cap: A$1,926.1m |

Source: Bloomberg

We rate PRY as a Sell due to the following reasons:

We see the following key risks to our investment thesis:

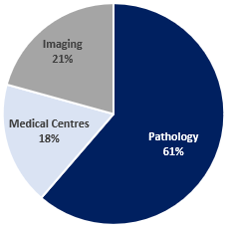

Figure 1: PRY Revenue Split by Segment

Source: Company

Figure 2: PRY EBITDA Split by Segment

Source: Company

Since our sell recommendation, the share price has declined -25%. In our view, although underlying NPAT was broadly in line with last year and with guidance, Primary Healthcare (PRY) delivered results which were disappointing given revenue was up ~4.9%, EBITDA down -9.3%, EBIT down -4.4%.

Free cash flow, before growth capital expenditure, was $146.6m, an improvement on FY17. Final dividend of 5.5 cps, 100% franked, on a payout ratio of 60% of Underlying NPAT. Further, PRY announced a $250m capital raising. Offer issue price is $2.50 per new share, a 17.8% discount to theoretical ex-rights price of $3.04 on 17 August 2018. Retail entitlement offer opens on 27 August 2018 and closes on 7 September 2018. PRY trading halt is lifted on 22 August 2018.

For investors currently in the stock, if the share price before the close on 7 September 2018, appreciates significantly beyond $2.50, we recommend take up and sell (to receive the benefit of the arbitrage). Overall, we maintain our Sell recommendation.

Figure 3: PRY Financial Summary

Source: Company

Figure 4: Peer group comparables – consensus

Source: Bloomberg

Figure 5: PRY Financial Summary

Source: BTIG, Company, Bloomberg

Primary Heath Care Ltd (PRY) operates 1) ~90 primary health care clinics in Australia. Its medical clinics are vertically integrated with family GPs, specialists, therapists; 2) ~90 pathology laboratories (along with ~800 specimen collection centres); and 3) over 160 diagnostic imaging centers. PRY offers different billing options through Medicare (Australia’s universal healthcare system) and bulk billing.