Analyst Research

14 August 2019

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 28/08/18 | TGR | A$4.50 | A$4.90 | BUY |

| Date of Report 28/08/18 | ASX TGR |

| Price A$4.50 | Price Target A$4.90 |

| Analyst Recommendation BUY | |

| Sector : Consumer Staples | 52-Week Range: A$3.44 – 4.68 |

| Industry: Packaged Foods & Meat | Market Cap: A$786.8m |

Source: Bloomberg

We rate TGR a Buy for the following reasons:

We see the following key risks to our investment thesis:

Figure 1: TGR revenue by markets

Source: Company

Figure 2: TGR revenue by segment

Source: Company

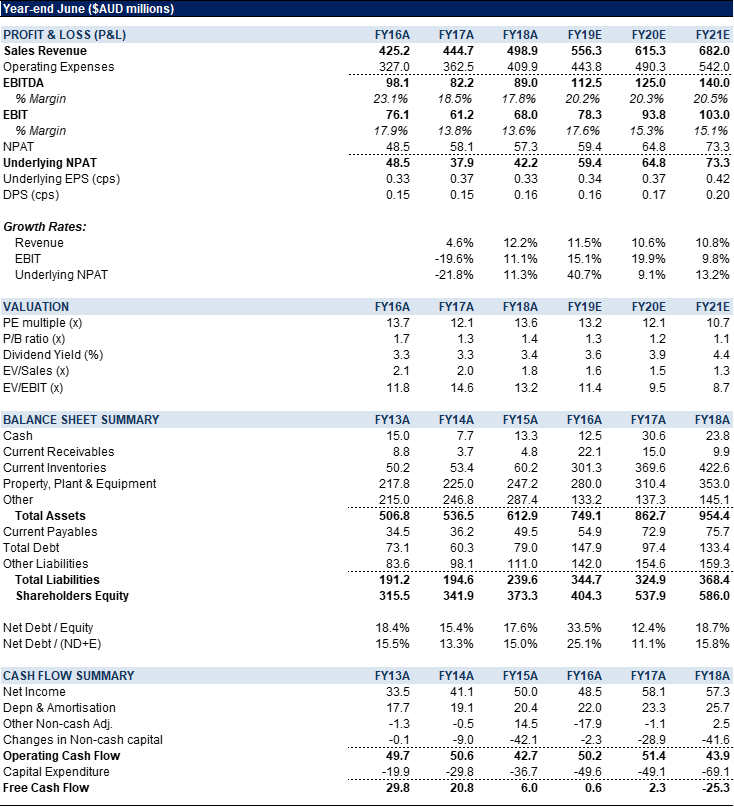

TGR’s FY18 operating profit of $50.3m and operating EBITDA of $99.78m came in below consensus estimates of $51.2m and $105.5m respectively.

The share price showed marginal improvement as investors focused on underlying growth in operating profit and EBITDA of +19.2% and +12.2%, respectively, and management stating, “there appears to be a supply shortage for domestic market fulfilment, and this should lead to strong pricing returns and an improved domestic pricing outlook”.

TGR announced the acquisition of Fortune Group’s prawn aquaculture business and the lease of a Well Boat.

Looking forward, we expect average prices to recover in FY19 on lower volumes in export and domestic market.

We maintain our Buy recommendation, given the upside to our current price target. On our estimates, TGR is trading on a FY20E PE-multiple of 12.1x and offering a fully franked yield of ~3.9%..

Figure 3: TGR FY18 key performance numbers

Source: Company

FY18 results highlights. When compared to pcp: 1. Revenue was up +13.1%, operating earnings (EBITDA) up +12.2% and operating NPAT up +19.2%. 2. Group results were driven by strong demand for salmon, especially in wholesale markets with export volumes up +98.4%, partially offset by cost pressures. 3. Average fish size improved +15.4% to 4.5kg, from 3.9kg in pcp. 4. EBITDA was driven by strong consumer demand for salmon, which helped improve pricing conditions and allowed for further optimization of sales mix to maximize margins. 5. Gearing increased to 18.7% from 12.4% in FY17. 6. Operating cash flow of $43.9m was down -14.6% from $51.4m in FY17. 7. Fully franked final dividend of 8cps (up +6.7%) was declared, bringing the total dividend payout for FY18 to 16cps (up +6.7% from pcp

Figure 4: TGR domestic and global peer group trading multiples – consensus

Source: Bloomberg

Figure 5: TGR Financial Summary

Source: Company, BTIG, Bloomberg

Tassal Group (TGR) is Australia’s largest vertically integrated seafood/aquaculture company. Based in Tasmania, TGR is engaged in hatching, farming, processing, sale and marketing of Atlantic salmon and ocean trout. The company’s products are distributed in Australia, Japan and other international markets.