Analyst Research

14 August 2019

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 27/08/18 | VVR | $2.15 | $2.30 | BUY |

| Date of Report 27/08/18 | ASX VVR |

| Price $2.15 | Price Target $2.30 |

| Analyst Recommendation BUY | |

| Sector : Real Estate | 52-Week Range: A$1.94 – 2.28 |

| Industry: Retail REIT | Market Cap: A$1,560.4m |

Source: Bloomberg

We rate VVR as a Buy and believe the following key drivers of performance will see the stock outperform the market:

We see the following key risks to our investment thesis:

Figure 1: VVR Portfolio Properties by state

Source: Company (FY17)

Source: Company

VVR reported solid 1H18 results with distributable earnings of 6.99cps, a +2.8% uplift. In line with the 100% payout policy, the distribution was likewise 6.99cps

Net tangible assets of $2.20 per security was +6.2% higher than 1H17 (or adjusting for the 6.99 distribution, adjusted NTA was $2.13, which is higher than the $2, a year ago). With gearing of 32.5% remaining below the target range of 35-45%; interest cover ratio of 5.6x and drawn-debt 93% hedged for 3.9 years at weighted average cost of debt of 3.84%; this provides VVR with the firepower for potential debt-funded acquisitions (undrawn debt capacity is $192m with full utilisation of that capacity increasing gearing to 37.7%).

VVR continues to manage operating cost well with a management expense ratio of 21 basis points (one of the lowest in the sector and reflective of the nature of the Triple Net leases to major tenant Viva Energy Australia). Trading on a 14.1x PE20, 7.0% dividend yield and 0.9x Price to Book – reiterate Buy.

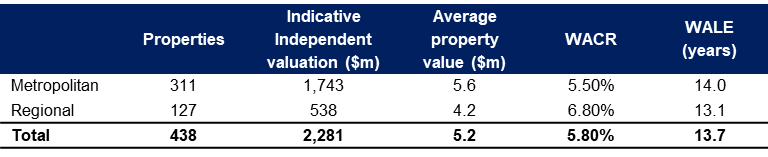

Figure 3: VVR Portfolio Overview

Source: Company – 1. Includes six properties contracted to be acquired by Viva Energy REIT which were not settled as at 30 June 2017.

Figure 4: VVR Financial Summary

Source: Company, BTIG, Bloomberg

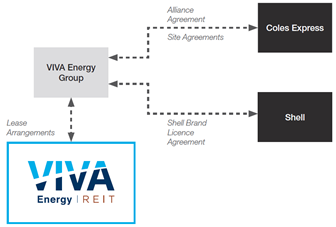

Viva Energy REIT Ltd (VVR) is an Australian listed REIT that owns a portfolio of service stations across all of Australia’s states and territories. It currently owns 437 service stations in its portfolio. Its service stations are leased on a long term basis to Viva Energy Australia who has licence and brand agreements with Shell and Coles Express. Average value by property is ~ A$5 million, with a weighted average cap rate of 5.9% and a WALE of 14.2 years (as of FY17).