News

22 April 2026

Dion Hershan, Head of Australian Equities, looks at why local investors might be inclined to ‘stay local’ in the year ahead.

This article was originally published on Yarra Capital Management. Reach Markets has permission from the author to publish it. The views and opinions expressed in this article are those of the author and do not necessarily reflect the views and opinions of Reach Markets.

Dion Hershan, Head of Australian Equities, looks at why local investors might be inclined to ‘stay local’ in the year ahead.

Australian investors are known to be very parochial, and have historically reflected this attitude with a home bias – possibly because of the lure of familiarity with companies, franking credits and the currency hedge (most spend in Australian dollars).

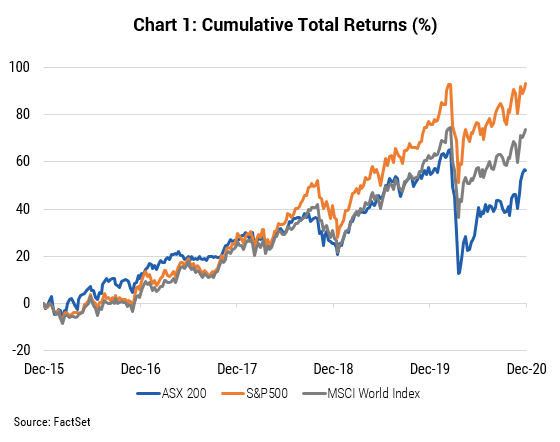

That domestic bias (with an over 50% allocation to Australian equities in our super1) has proved sub-optimal in recent years. Over the past five years the ASX has underperformed global markets by 2.4% p.a. and, in particular, the US market by 4.8% p.a.

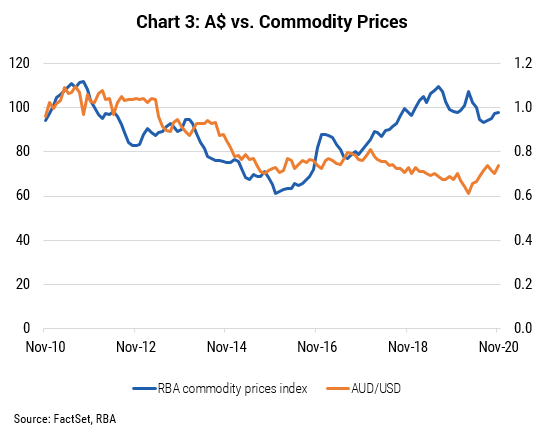

There is, however, a compelling tactical argument for ‘staying local’ over the next few years:

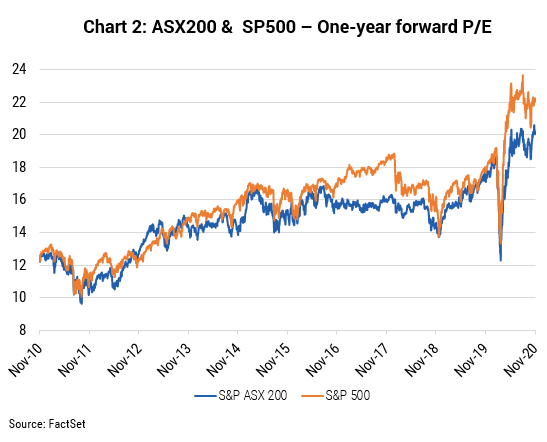

What is debatable, though, is how the sector composition of the Australian market will fare versus global equivalents. Its heavy reliance on banks (20%), REITs (7%) and resources (20%) means it has more ‘value characteristics’, particularly versus the S&P500 and its 28% weighting to Tech . I won’t dare wager into the ‘growth vs. value’ debate, but is an obvious point the Australian market is far more leveraged to ‘value’ and as such offers lower P/E multiples and higher yields.

We have positioned our portfolio accordingly, only owning a select few global businesses which we feel have exceptional prospects (e.g. Aristocrat Leisure, James Hardie). Instead we are significantly skewed towards the local economy – being overweight banks which will be a winner as bad debt levels recede – and domestic cyclical businesses including Reece, JB Hi Fi, Nine Entertainment and Bluescope.

On the 29th January Reach is joined by Joel Fleming, Portfolio Manager at Yarra Capital, for our monthly ‘Meet The Fund Manager’ webcast. If you would like to attend the session and have an opportunity to ask Joel questions live, you can book here.

‘Meet the Fund Manager’ is a monthly webcast series which gives you direct access to prominent fund managers who share their “Insider” views on their top stock picks that they think have the greatest upside.

[1] FTSE Russell: Appraising home bias exposure, October 2019

Past performance is not a reliable indicator of future performance.