Analyst Research

14 August 2019

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 27/08/18 | MPL | A$3.03 | $3.44 | BUY |

| Date of Report 27/08/18 | ASX MPL |

| Price A$3.03 | Price Target $3.44 |

| Analyst Recommendation BUY | |

| Sector : Financials | 52-Week Range: A$2.79 – 3.39 |

| Industry: Life & Health Insurance | Market Cap: A$8,344.6m |

Source: Bloomberg

We rate MPL as a Buy for the following reasons:

We see the following key risks to our investment thesis:

Figure 1: Population growth and Participation rate

Source: Company

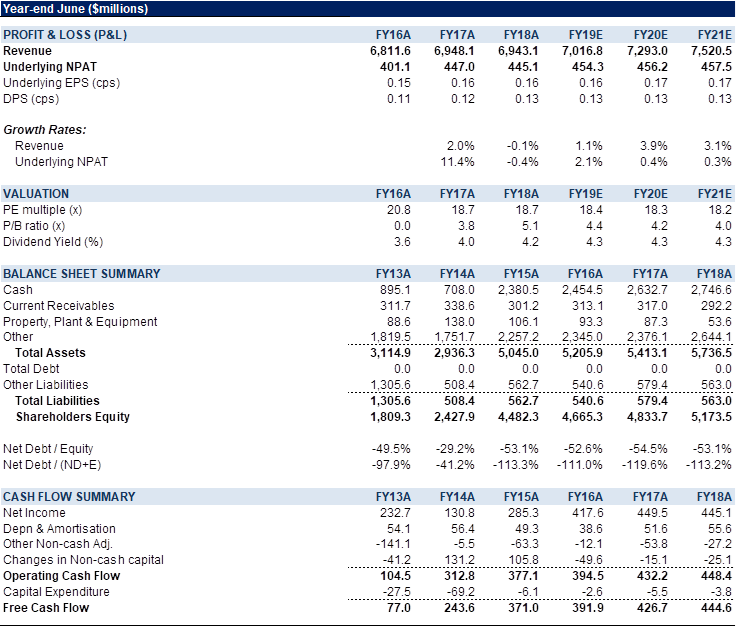

Medibank Private (MPL) reported FY18 results with NPAT of 445.1m and EPS of 16.2cps, both of which came in below market estimates of $453.8m and 16.7cps respectively, dragging the share price down by -2.2% at the close.

Given the industry is facing issues of customer affordability, we think the health insurance business performed well delivering revenue of $6.3bn up +1.2% over pcp. Group NPAT of $445.1m, down -1% from $449.5m in FY17 with solid results from Medibank Health offset by lower net investment income (lower equity and credit market returns) however, group EBITDA rose +9.7% to $548.8m.

Management noted that market share grew by 5bps over the past 6 months. MPL delivered a dividend at 80% of NPAT. Operating profit increased +32.5% and gross margin improved 110bps.

We remain concerned over short term issues such as affordability of private health insurance (and hence policyholder growth numbers) that all private health insurers are dealing with.

MPL is currently trading on reasonable ~18.3x forward P/E, 4.3% yield, attractive ROE of ~25% – we are cognizant of short-term challenges, but longer term, we don’t doubt the quality of MPL. Reiterate Buy.

Figure 2: MPL FY18 Results Summary

Source: Company

Figure 3: MPL Financial Summary

Source: Company

Medibank (MPL) is Australia’s largest private health insurer with ~30% market share. Medibank’s health insurance business (Health Insurance) underwrites private health insurance and the insurer generates revenue from a number of complementary services.