Analyst Research

14 August 2019

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 27/08/18 | VOC | A$2.79 | A$2.59 | NEUTRAL |

| Date of Report 27/08/18 | ASX VOC |

| Price A$2.79 | Price Target A$2.59 |

| Analyst Recommendation NEUTRAL | |

| Sector : Telecommunication Services | 52-Week Range: A$2.11 – A$3.33 |

| Industry: Integrated Telecommunication Services | Market Cap: A$1,735.9m |

Source: Bloomberg

We rate VOC as a Neutral for the following reasons:

We see the following key risks to our investment thesis:

Figure 1: Revenue split by segments

Source: Company (FY17)

Source: Company

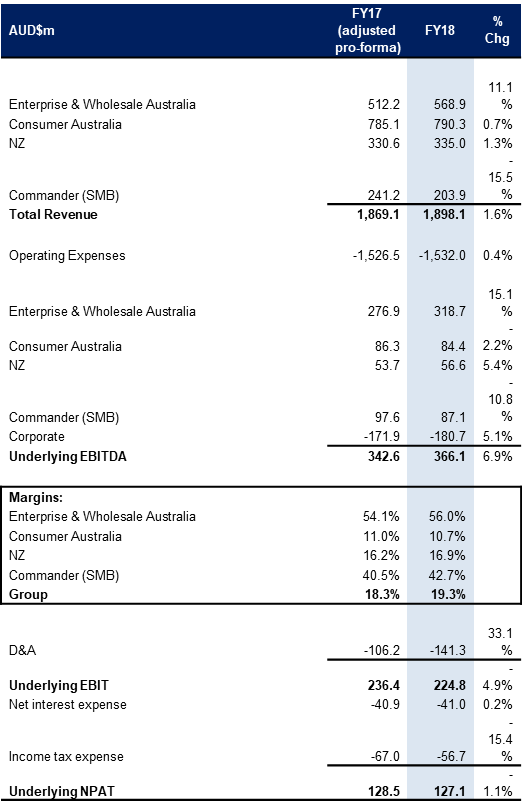

VOC’s FY18 results came slightly below consensus estimates, with underlying EBITDA of $366.1m (below market estimate of $369m), revenue of $1.898bn (below estimate of $1.936bn) and underlying NPAT of $127.1m (below estimate of $127.72m).

However, in our view, the results are solid considering significant internal changes going on in VOC and headwinds from overall challenging market conditions. The cash conversion improved significantly from 52% in FY17 to 88% in FY18 and VOC refinanced debt increasing the weighted average tenure to 3.4 years with net debt of $1bn at the end of the year.

Management confirmed the completion of Australia Singapore Cable by September 2018. There were new appointments across the executive team, including the appointment of a new CEO and two new executive directors.

At this stage we continue to maintain our Hold recommendation despite clearly seeing value in the stock from a valuation perspective relative to peers (which is warranted, in our view as we await further indications that the new management team is executing on strategy.

Figure 3: VOC FY18 key headline numbers

Source: Company

Figure 4: VOC Financial Summary

Source: Company, BTIG, Bloomberg

Vocus Group Ltd (VOC) is a vertically integrated telco provider operating in Australia and New Zealand. VOC primarily provides telco and energy services to customers across its mass market, corporate and government channels through its extensive national infrastructure network. This network consists of metro and back haul fibre connecting all capital cities and most regional centres across Australia and New Zealand.