Analyst Research

14 August 2019

| Date of Report | ASX | Price | Price Target | Analyst Recommendation |

| 23/08/18 | CWY | A$2.05 | A$2.12 | NEUTRAL |

| Date of Report 23/08/18 | ASX CWY |

| Price A$2.05 | Price Target A$2.12 |

| Analyst Recommendation NEUTRAL | |

| Sector : Industrials | 52-Week Range: A$1.30 – 2.08 |

| Industry: Waste Management | Market Cap: A$4,176.0m |

Source: Bloomberg

We rate CWY as a Neutral for the following reasons:

We see the following key risks to our investment thesis:

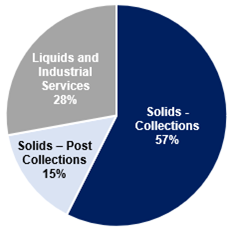

Figure 1: Revenue by Segments

Source: Company

CWY reported strong FY18 results amidst changing regulatory environments in National Sword Policy and Recycling, with organic growth experienced across all segment revenues, earnings (EBIT) and margins.

Key highlights included: 1. Underlying net revenue up +15.9% to $1564.9m. 2. Underlying EBITDA up +12.7% to $339.7m. 3. Underlying EBIT up +16.4% to $166.4m. 4. Underlying NPAT up +26.2% to $97.8m. 5. Cash flow performance was strong with operating cash flow up +16.7% and free cash flow up +86.6%.

The acquisition of Toxfree Solutions has been completed and Management reiterated that it will deliver ~$35m in synergies over 2 years. Whilst no quantitative guidance was provided by CWY, management did provide positive comments on CWY’s future earnings profile.

We have no doubt about the quality of the management team and assets and that CWY should provide consistent and stable returns (barring any unforeseen issues), however, we reiterate our Neutral recommendation on valuation grounds.

Figure 2: CWY Results Overview – Group level (Underlying Results)

Source: Company

Figure 3: CWY Financial Summary

Source: Company

Cleanaway Waste Management Ltd (CWY) is Australia’s leading total waste management services company. CWY has a nation-wide footprint in solid, liquid, hydrocarbon and industrial services (with ~200 solid, liquid, hydrocarbon and industrial services depots and processing facilities across the country servicing well over 100,000 customers. CWY operates three core segments: (1) Solids (Collection) operates the largest network of collections vehicles in Australia operating from more than 100 depots, servicing 90+ municipal councils; (2) Solids (Post Collections) has one of the largest post collections asset bases in Australia with a growing network of transfer stations and landfill assets; (3) Liquids & Industrial Services encompasses the largest hydrocarbons recycling business in Australia.